Managing money can be challenging when your paychecks don’t look the same every month. Whether your income fluctuates due to seasonal work, hourly wages, commission, or irregular hours, you can build a reliable budget that works—with the right system in place.

In this guide, we’ll break down a practical paycheck budgeting strategy that helps you cover bills, build savings, and plan for future expenses even when your income changes.

Simple System That Actually Works

📌 Why Budgeting with Irregular Paychecks Matters

Living without a consistent paycheck can feel unpredictable, but budgeting isn’t out of reach. A solid plan helps you:

Track income and expenses more accurately

Avoid surprises when bills are due

Save for emergencies and future goals

Reduce stress around money decisions

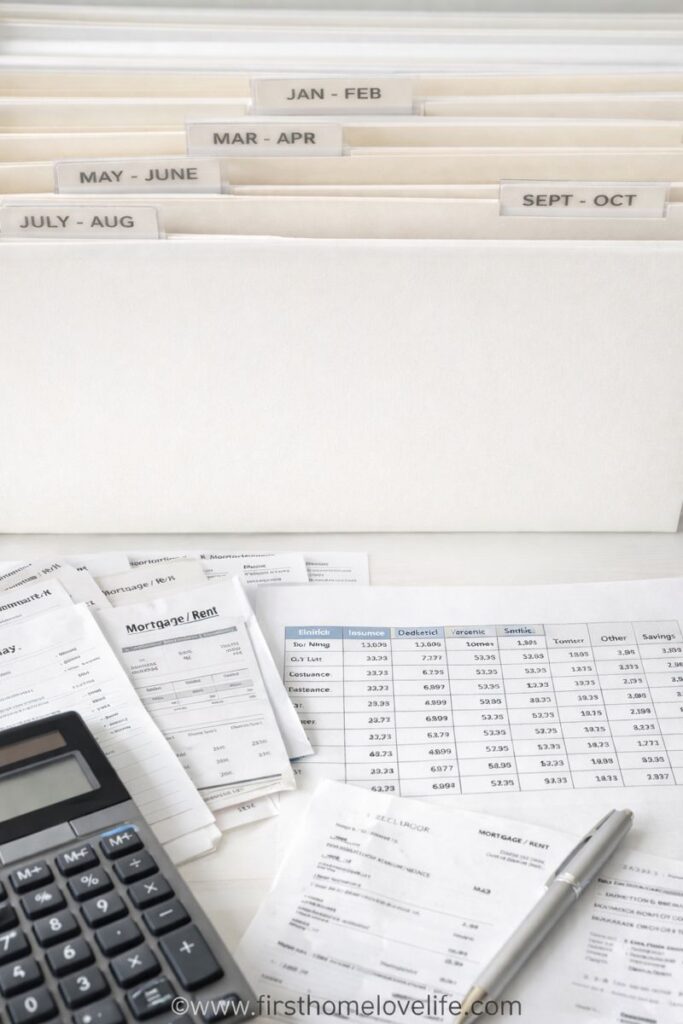

📊 Step 1: Analyze Last Year’s Bills

Start by gathering all of your past bills—electricity, water, rent, insurance, etc.—and organize them by month. This helps you identify patterns in spending and estimate yearly costs even if your income changes month to month.

🧮 Step 2: Calculate Your Average Cost

Once you have a year’s worth of bills, add them together and divide by 12 to get your monthly average. This average gives you a baseline for planning—even if your paycheck sizes change.

If you’re paid biweekly, divide that average by 2—and that number becomes the amount you should set aside from each paycheck to cover bills throughout the year

💼 Step 3: Set Up a Dedicated Bill Account

One effective budget method is to transfer the calculated amount from every paycheck into a designated bill account. This account is used only for paying monthly bills so you avoid spending that money on anything else.

This strategy helps prevent cash flow gaps and ensures your regular expenses are paid on time—even when income varies.

💰 Step 4: Allocate the Rest

After you’ve funded your bill account, divide the remaining money from each paycheck into savings, emergency funds, groceries, and “fun money” categories. Treat every dollar like it has a job—whether it’s covering needs or building your financial goals.

🔁 Step 5: Overfund When Possible

In months when your income is higher than usual, add extra to your bill account or savings. This creates a cushion you can rely on during leaner months.

💡 Bonus Tips for Budgeting with Variable Income

Track how much you actually earn over several months before setting your baseline.

Use budgeting tools or spreadsheets to monitor trends.

Prioritize essential expenses first and make adjustments as you go

📌 Summary: Budgeting Strategies that Work

Budgeting when paychecks differ doesn’t have to be overwhelming. By understanding your spending patterns, calculating average costs, and setting up a dedicated bill-paying system, you can create a flexible and reliable budgeting system that works even with an irregular income.